The Return of Japan

Portfolio Manager Shuntaro Takeuchi explains how rising inflation and volatile markets may cast Japan as an investment haven, with a breadth of hidden value available to be tapped.

Japan perplexes and inspires. Perplexes because of its decades-long efforts to stimulate growth and spending and inspires because of the efficiencies and capabilities of its manufacturing and technology industries.

It’s easy to write Japan off as an ex-growth play given its decades of muted economic growth. But that would be to mix Japan’s GDP performance with the performance of Japanese corporate profits. Japanese earnings have in fact improved significantly over the past decade and in today’s volatile markets and inflationary environment Japanese stocks may be on the cusp of providing a compelling combination of attractive valuations and growth opportunities for investors.

In addition, the traits of the nation’s aging population and the demographic demands that Japanese companies have worked so hard to satisfy over the years are now presenting themselves in other countries. This gives Japanese corporates the opportunity to step into overseas markets with ready-made business models.

Hidden Value

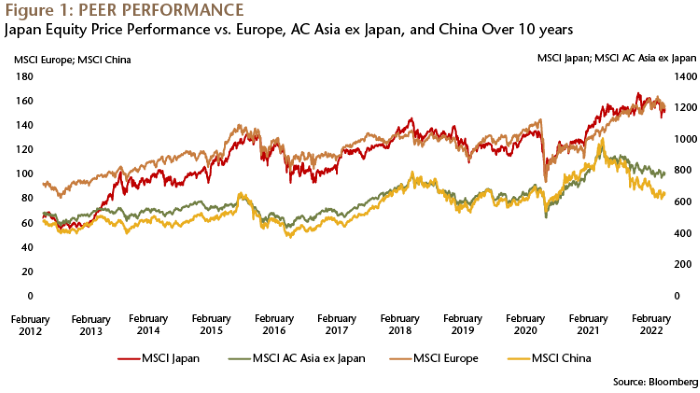

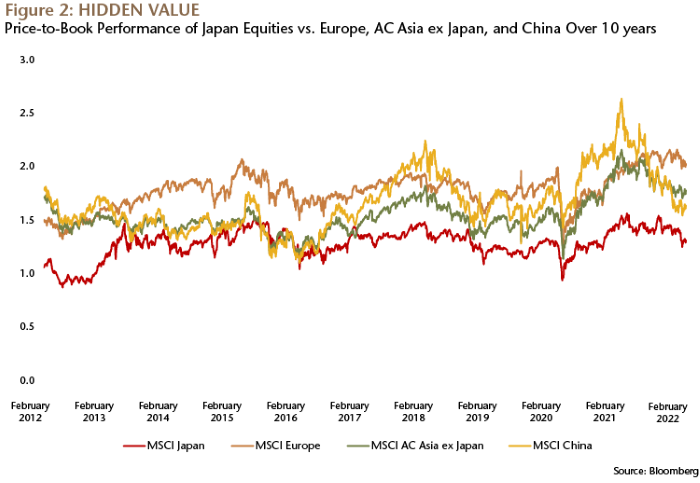

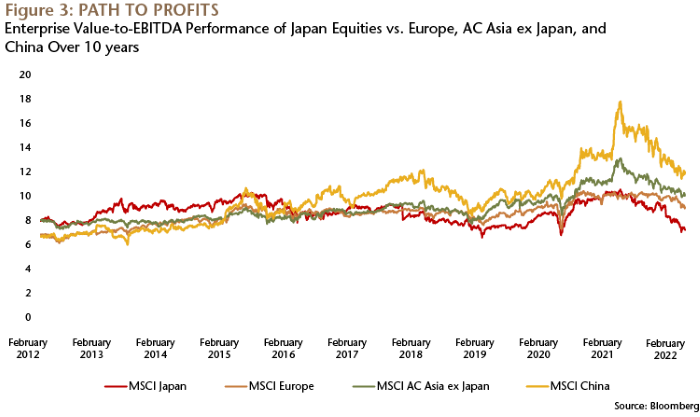

The first reason we think Japan is beginning to show itself as something of an investment haven is valuation. The charts show how the MSCI Japan Index (“Japan”) has fared compared with the MSCI Europe (“Europe”), the MSCI AC Asia ex Japan (“Asia ex Japan”) and the MSCI China (“China”) indices, in terms of stock price, price-to-book ratio (P/B) and enterprise value-to-ebitda ratio (EV/ebitda) ratio over the past 10 years.

Investment involves risk. Past performance is no guarantee of future results. Indices are unmanaged. It is not possible to invest directly in an index. This information is presented solely for illustrative purposes and is not representative of the results of any particular security or product.

Investment involves risk. Past performance is no guarantee of future results. Indices are unmanaged. It is not possible to invest directly in an index. This information is presented solely for illustrative purposes and is not representative of the results of any particular security or product.

Investment involves risk. Past performance is no guarantee of future results. Indices are unmanaged. It is not possible to invest directly in an index. This information is presented solely for illustrative purposes and is not representative of the results of any particular security or product.

While growth in Europe, Asia ex Japan and China has been supported by multiple expansion, the appreciation of Japan stocks has been mainly through earnings performance. The average P/B ratio over the past 10 years in Europe was 1.8x, in Asia ex Japan it was 1.5x, in China it was 1.6x, and in Japan it was 1.3x.

Over the past decade, Japan’s earnings growth and general improvements in cash flow generation—thanks mainly to innovation, productivity and capital efficiencies—have not been reflected in valuations compared with its peer markets.

So, what does this mean in a global era of rising prices and tighter monetary policy?

As we know, in periods of inflation and rising interest rates there tends to be downward pressure on equity multiples as growth investors seek “safer” assets at a higher yield elsewhere. In Japan, that downward pressure is diffused given that it is an equities market where valuations are at the bottom of the range. We’re not saying Japan is poised to outgrow its peers in terms of absolute earnings growth rates but earnings growth rates are comparable with peers and it offers much more generous valuations levels, in our view.

Cyclical Recovery

The second factor that could emerge in Japan’s favor is the possible fading of the value investing rally. This view may seem contrarian given the aggressive value run in Japanese indices in recent months. However, the switch to value can be seen as a countering trend to the extent that it followed a period of outperformance by growth stocks on the back of a rally in equity markets in 2020 as pandemic vaccinations started to emerge.

In addition, ahead of potential rate rises by the Federal Reserve, we tend to see a move to value stocks as investors seek out companies that are profitable now. Historically, when rates have begun to rise, value rallies have tended to subside. In this phase, growth stocks, particularly in cyclical sectors, can recover. So once the dust settles after the Fed starts to hike, we may see quality Japanese companies in cyclical sectors like manufacturing, autos and technology becoming more attractive. This trend, combined with solid earnings growth rates, would potentially provide a driver for Japanese equity prices.

A word here on growth investing in times such as these when value investing still prevails. Successful growth investing right now requires digging deeper. In an inflationary environment alongside tightening monetary policies in the U.S. and the West, we believe investors can no longer sit on high growth names trading at high multiples. Instead, we believe a balanced approach with a mix of cyclical growth stocks, idiosyncratic growth stocks (where potential growth is based on company-specific traits), and turnaround stocks (where growth potential is locked into a recovery strategy) should be considered.

Exporting Business Models

The third potential driver for Japan equity returns are Japanese companies themselves, which are used to having to make headway, domestically at least, in the face of fairly flat consumer demand, an aging population and land use that is at a premium. These conditions have worked to nurture innovation and efficiencies at Japan’s conglomerates and at its smaller companies—across traditionally powerful sectors like technology, health care and manufacturing and new growth sectors like electric vehicles, battery production, automation and renewable energy.

Some of these social-economic and demographic traits are now becoming more entrenched in other economies, offering Japanese companies an opportunity to parlay their business models overseas. Health care is one example. Owing to Japan’s aging population, the country has an advanced medical devices industry tailored to supplying products like catheters and plastic syringes that help maintain the health of Japan’s elderly population and enable health-care providers to make substantial cost savings. Medical device manufacturers that produce plastic syringes with advanced coatings to preserve drug quality, for example, are now competing head on with incumbent players in overseas markets.

Another example is instrumentation manufacturers. Until recently, these firms got almost all their revenue from the domestic Japanese market as clients, like chip manufacturers, sought to make their existing plants more effective. Now, premiums on factory space and factory costs are being felt in overseas markets like the U.S. and China, and Japanese component suppliers are leveraging their domestic expertise to exploit these opportunities.

Industrial Prowess

And regardless of macro environment and socio-economic trends, the prowess of Japanese businesses should never be underestimated. Japan is now home to some of the market leaders in electric compressors—instruments that support air conditioning systems in electric vehicles (EVs). Its auto companies have entered into EV production and will be in a position to provide EVs for large sections of the population. Japan’s powerful consumer gaming and entertainment sector is getting ever stronger, securing lucrative intellectual property (IP) rights and leveraging changing consumer demands driven by technological change like music streaming.

From a structural point of view, the earnings capability of Japanese companies has improved meaningfully over the past economic cycle, driven by better corporate governance and a higher focus on capital efficiency. Long-term trends such as productivity growth, health care, technology and materials science innovation remain intact and now offer a breadth of hidden value to be tapped.

As global inflation looks poised to curtail the growth trajectories of some of Japan’s market peers, investors should be cognizant to the strength and quality of Japan’s corporate earnings and the potential for unlocking value.

Definitions

The MSCI Japan Index is a free float–adjusted market capitalization–weighted index of Japanese equities listed in Japan.

The MSCI Europe Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the developed markets in Europe.

The MSCI All Country Asia Pacific Index is a free float-adjusted market capitalization–weighted index of the stock markets of Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan and Thailand.

The MSCI China Index is a free float-adjusted market capitalization-weighted index of Chinese equities that includes H shares listed on the Hong Kong exchange, B shares listed on the Shanghai and Shenzhen exchanges, Hong Kong-listed securities known as Red chips (issued by entities owned by national or local governments in China) and P Chips (issued by companies controlled by individuals in China and deriving substantial revenues in China), and foreign listings (e.g. ADRs).

Price to Book Ratio (P/B Ratio)—P/B Ratio is used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share. A lower P/B ratio could mean that the stock is undervalued.

Enterprise Value-to-Ebitda Ratio—EV/EBITDA (Enterprise Multiple) is a ratio used to determine the value of a company. The enterprise multiple looks at a firm as a potential acquirer would, because it takes debt into account—an item which other multiples like the P/E ratio do not include.