Why Asia Matters

CIO designate Sean Taylor gives his take on what Asia has to offer global and emerging markets investors, from growth, to diversification, to innovation.

Key Takeaways

- Most Asia markets, like many emerging markets elsewhere in the world, have emerged from COVID with their finances intact and poised to transition into easing cycles that will foster growth.

- India, Japan and China, Asia’s power houses, offer considerable investment opportunities in their own ways—both near and long term.

- Markets are interconnected. While individual markets can offer their own particular strengths, like India and Japan, getting exposure to good companies across Asia and emerging markets, in our view, is the way to leverage the economic momentum of these regions.

As San Francisco, home to Matthews’ U.S. headquarters, closes hosting the Asia-Pacific Economic Cooperation (APEC) meetings this year, it’s worth reflecting on the role Asia plays in the global economy, in emerging markets and in our portfolios. In short, Asia matters. It remains the growth engine of the world. It’s an important part of global supply chains. Asia has innovation and growing consumption and it is increasingly important as a trade area itself. Above all, Asia matters because it continues to grow and is projected to grow faster than any other region in the coming years.

From a portfolio standpoint, Asia is also a diversifier. It offers diversification from other regions such as the U.S. and it offers differentiation across different markets within itself. Asia is also becoming more institutionalized. It has a growing domestic investment culture; it has more Asian investors and more domestic pensions funds, sovereign wealth funds and mutual funds.

This all said, these have not been easy times for investors. Within Asia’s constituent parts, China’s economy has faced challenges and its equity markets have not performed well. And when China slows others slow, like Thailand which depends on China for tourism and trade. Indonesia and Australia, big exporters of commodities to China, have also felt the pain. At the macro level, the Federal Reserve’s interest rate strategy and the strong U.S. dollar have also been a headwind for Asia and emerging markets generally. At the same time, we have also seen some good individual equity market performances. India and Indonesia—the latter in spite of its significant commodity exports to China—have both done well. Elsewhere, parts of South Korea and Taiwan have performed, particularly in the technology sector.

“When the Fed finally pauses from its ‘higher-for-longer’ strategy and Asia markets also loosen, this should provide a growth tailwind.”

Asia—and Latin American markets—have also shown their macro stripes in these challenging times. In LatAm, central banks raised their rates ahead of the Fed and are now embarking down a path of looser monetary policy. While inflation has been less of an issue in Asia, its central banks also tightened appropriately. When the Fed finally pauses from its ‘higher-for-longer’ strategy and Asia markets also loosen, this should provide a growth tailwind.

Looking ahead, we think Asia has a lot to play for. It has markets which are industrializing and creating capital to invest in infrastructure like India, Vietnam and Indonesia. And it has consumer markets that are moving from staples to discretionary and are digitalizing on a rapid scale. It also has markets like South Korea and Japan with low growth, but which play crucial roles in global technology supply chains. And, dare I say it, when China’s growth picks up that will not only be good for China, it should have a cascading effect across its trading partners in Asia and global emerging markets.

Which brings me back to APEC, which gathered leaders from 21 member economies in and outside Asia that account for nearly 40% of the world’s population and nearly 50% of global trade. It’s true that a lot of the strength of Asia derives from its individual markets, but the reality is that markets across the world are interconnected. The prospects of mining companies in Brazil and battery makers in China, for example, are intertwined. Often with such global events, the optics are more memorable than the things that get done at them. But world leaders talking to each other can only be a good thing for our planet, for addressing poverty, for global relations, and for trade and wealth generation.

Here's a closer look at the prospects and trends for some of our key markets:

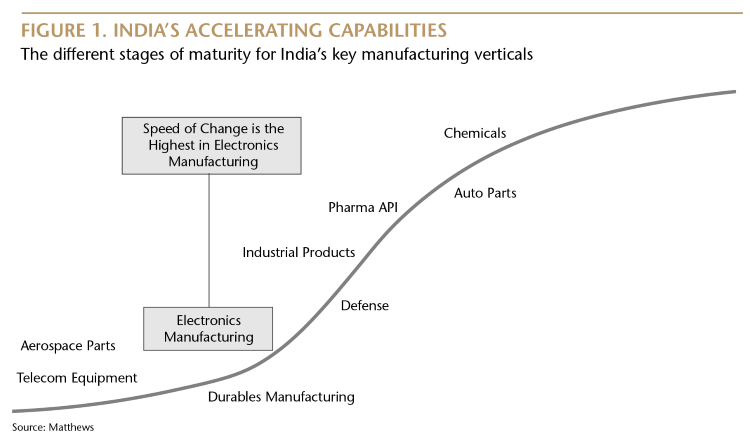

Made in India

Portfolio Manager Peeyush Mittal

People often talk about India benefiting from being an attractive alternative to China as a manufacturing or operating hub for global companies. But in my view the ingredients for India’s growth have been in place for some time.

In the years before the pandemic, the Modi government started to prioritize making the country more pro-business by reforming tax laws, improving transport and infrastructure and increasing the efficiency of land acquisition. Since COVID, this has continued with an increased focus on fostering domestic manufacturing and innovation.

As a result, companies from chemicals, pharmaceuticals and auto parts to increasingly electronics, manufacturing and aerospace parts, are expanding in India. Consumer durables is one such space where domestic manufacturing is substituting imports from China. The Indian government has encouraged overseas companies and multinationals to come to India and this strategy has been helped by global negativity toward China. But there are India-centric reasons why India is attractive to foreign companies. India now has a large and powerful consumer market and, importantly, higher-value discretionary spending, such as on cars, travel and recreation, is a rapidly expanding component.

While there’s a lot of runway for India, we are also cognizant of India’s challenges. Investors need to know India, where it has come from and where it’s going. From a governance point of view, there is still work to be done in terms of diversity, equality and regarding shareholder transparency and accountability. There are also some rich valuations and the outlook for India is heavily influenced by global variables, like persistent high interest rates in the West that may challenge Indian exports.

Japan’s Upside

Portfolio Manager Shuntaro Takeuchi

The performance of Japan’s equity markets year-to-date has been strong, fueled by corporate profit growth, a positive earnings cycle driven by moderate inflation and a recovery in inbound tourism, as well as improving corporate governance. Of these tailwinds, governance reforms, aimed at increasing the capital efficiency of Japanese-listed equities, may become a notable attribute of the market going forward.

(Downtown Tokyo)

Over the past 10 years, corporate Japan’s cash on the balance sheet has grown more than five-fold amid strong earnings, however, companies have tended to hold onto this cash and valuations have suffered. This year, the government instructed Japanese firms to improve their capital efficiency, as measured by return on invested capital (ROIC) and return on equity (ROE), and in response many companies have increased stock buybacks and raised dividend payouts. This development has significantly boosted the potential upside in total return profiles of Japanese companies, in our view. The capital efficiency reforms have a long way to go but they should ultimately lead to equity-multiple expansion in Japan that has been absent over the past 15 years.

Looking at the bigger picture, what has hampered investor sentiment toward Japanese equities in recent years has been the perception that Japanese corporate profits are tied to Japan’s macro profile of low gross domestic product (GDP) growth, low wage growth, and near zero inflation. But these macro variables are also changing. And while concerns are gathering over a global slowdown we think recovering demand in China will offer a meaningful outlet for Japanese exports. With the yen at a near quarter-century-low to the dollar, inflationary growth seemingly bedding in, and corporate reforms gaining traction, we think the case for Japan is now a powerful one.

China’s Challenge

Portfolio Manager Andrew Mattock

China remains challenging. Of its three economic drivers, property and manufacturing are having a tough time while the other, domestic consumption, is in low gear. On a note of optimism, the cadence of policy announcements aimed at supporting China’s property market and domestic consumption is encouraging. In terms of U.S.-China relations, amid the serious conflicts in the world there are encouraging signs that the two global superpowers are re-opening of lines of communication, the latest example being the meeting of President Biden and Xi Jinping at the APEC summit.

In this environment we have to stay locked in to what matters for us. Next year, Chinese company earnings are projected to increase by 16% and if this comes to fruition, absent any deterioration in geopolitics and assuming the Chinese economy continues to recover, we should be looking at potentially positive equity returns.

But we aim higher than this. Our view has always been that China is a vast market with lots of opportunities for the active investor and we go in search of these. We look at Chinese companies listed on the Hong Kong and U.S. markets, for example, many of which are growth businesses with bright futures, like fintech, e-commerce platforms, fast food chains and travel service companies. We also look at companies listed on China’s mainland markets that have more exposure to domestic industry and manufacturing as well as supply chains. That’s an engine can help drive portfolio returns if recovery in China’s domestic economy takes hold.

Investing in Mega Trends

Portfolio Managers Elli Lee and Michael Oh

It's difficult to comment on technology and innovation without acknowledging the world-class companies within South Korea and Taiwan.

South Korea is a fast-paced environment. You can see it in daily life. Robots seem to be everywhere—in restaurants, in stores, in homes. South Korea always seems to be innovating. It’s one of the few markets globally where U.S. e-commerce and search companies don’t have dominancy.

Then there are global technology supply chains. South Korea dominates the market for DRAM (dynamic random-access memory) semiconductors. The market has consolidated over the past two decades and now South Korea has 70% share of global production. South Korea is also a major producer of electric vehicle (EV) batteries and has the second-largest share of the market behind China.

Taiwan is another core innovation hub in Asia. In addition to its chip industry, over the past 20 to 30 years, Taiwan has built up a massive moat in PC and server manufacturing. These companies are hardwired into global computing technology supply chains and are not easily replaceable. Taiwanese—and South Korean companies—have also tapped into the nascent artificial technology (AI) sector and are becoming crucial cogs in the supply chain.

While Taiwan and South Korea are plugged into the world economy and are sensitive to industry cycles and global downturns, they are also embedded in the world’s mega trends, like AI, robotics, new energy, internet services and health care. In our view, South Korea and Taiwan are part of the backbone of global innovation that will help shape and drive the world economy.

Global Emerging Markets in Perspective

Portfolio Manager Alex Zarechnak

There are three ways to look at investing in emerging markets, in my view. First, there’s the ‘snapshot’ where the negatives, like military conflict or geopolitics, are often front and center and the good news tends to be in the background.

Then there’s the ‘movie’, the ongoing story of emerging markets the asset class. In the 1990s, investing in emerging markets was about investing in fragile countries; buying countries that were in a boom phase while avoiding those that were going to crash. Today, these markets, in my view, are more stable as their monetary and fiscal capabilities and coordination have improved significantly.

This is where the third way to look at emerging markets comes in which I call the ‘truth’. The truth is the insights we uncover about quality companies in emerging markets and how we can get the best from them as investors. When markets are functioning more or less normally, private sector companies are usually geared toward solving societal issues, and in doing so create value for themselves and for their shareholders.

Today, emerging markets in and outside Asia contain many great companies with solid business models and quality management. We also see emerging markets as an interconnected landscape. EV batteries are a good illustration. You have the raw materials like copper and lithium sourced in Latin America that feed into the manufacture of the batteries in China and South Korea—that’s a fast-growing market opportunity tied to just one end-product.

Sean Taylor

Chief Investment Officer Designate

Matthews Asia